Are you worried about securely connecting and sharing data from your financial institutions with the apps you choose? Then you need plaid as a solution to your financial problems. Follow this article for all that you need to know about what is plaid banking and how to use plaid banking for bank transfers

Plaid banking has emerged as a transformative force in the rapidly evolving financial technology landscape, revolutionizing how consumers connect with their banks, financial apps, and services. Plaid is a leading fintech company that acts as a secure intermediary, facilitating seamless connections and data transfers between financial institutions and various applications.

At its core, Plaid Banking leverages powerful application programming interfaces (APIs) to enable users to access and share their financial information securely. By bridging the gap between consumers and fintech platforms, Plaid empowers individuals to connect their bank accounts to various services, such as budgeting apps, investment platforms, lending services, and more.

The key strength of Plaid lies in its ability to aggregate data from different financial institutions, offering users a holistic and consolidated view of their financial lives. This comprehensive perspective allows individuals to make informed decisions, manage their money more effectively, and better understand their financial well-being.

Moreover, Plaid banking is crucial in driving innovation within the financial industry by simplifying and standardizing the data-sharing process. Plaid paves the way for new and exciting financial services to emerge, enhancing accessibility and expanding consumer possibilities.

In this article, we will delve into the intricacies of Plaid Banking, exploring its significance, functionalities, and benefits to both consumers and the financial ecosystem. Join us on this journey as we uncover the transformative power of Plaid and its role in shaping the future of financial connectivity.

What is Plaid?

You may have encountered Plaid by installing and registering for a financial app, such as a budgeting tool, a payment app, or a wealth management program. Plaid is a fintech business that securely connects clients with financial service providers with apps.

Banks and other financial service providers use Plaid to give an additional degree of protection to their consumers when utilizing financial apps. Plaid’s services are generally free for the consumer because the financial service provider pays a charge to use Plaid in the first place.

Plaid is technically a platform with a set of technologies that allows developers to create financial applications that can communicate with bank accounts, perform payments, and manage risk. It enables users to simply authenticate and link their bank account to any application and access bank-like functions from that app. Plaid allows you to create applications that sync with users’ bank accounts to track and manage their budgets and transfer payments.

It acts as a bridge between banks and financial technologies. Several well-known firms use Plaid’s products and solutions, including Gusto, Venmo, TransferWise, Charity Water, Robinhood, and Level Money. Gusto, a prominent integrated online HR service, powers its payroll direct deposit service with Plaid’s automated clearing house (ACH) capabilities.

Image Source: TechCrunch

Other fintech companies, such as the budgeting tool Level Money, use the platform to combine and clean data from users’ several bank accounts to help them manage and budget their money.

Plaid, in a broad sense, covers essential parts of financial services such as payment setup and financial data validation.

It can assist you in organizing and executing ACH payments, collecting transaction data, validating user identity, examining job and income data, assessing user riskiness, and embedding bank interfaces directly inside borrower flows. With Paid, creating your own application has never been easier – with only a few lines of code; you can include Plaid into whatever you’re working on.

The front-end module of your app’s interface is straightforward and uncomplicated, making it easy for users to understand how to utilize it. Six products are available from Plaid, which include transactions, assets, auth, balance, income, and identity.

Each of these products produces data that may be utilized to enhance the user experience, and they all make access easier through a single integration. The platform enables users to construct and adapt solutions per their requirements, whether for business finances, personal finances, consumer payments, loans, or banking and brokerage.

How did Plaid come into being?

Plaid was started in 2013 by Zach Perret and William Hockey. The two initially tried to develop budgeting and consumer financial management software, including bookkeeping. They chose to alter their principal area of company attention to a unified banking API after experiencing difficulties establishing the required bank account connections for these tools.

The founders departed Atlanta for New York. They slept on friends’ couches for the better part of 18 months while developing the new idea. The fresh college graduates had been coding for years. Hockey, now 31, began at 12 as he was servicing neighbors’ computers in California as a hobby. At the same time, Perret picked it up in his late teens. The two created an initial Plaid prototype and secured enough funds to proceed and “develop, heads down,” for 20 hours.

Image Source: CNBC

According to them, the TechCrunch hackathon was the first time a team constructed a full-scale financial services application in less than 24 hours. After they won, “many people started paying notice,” including venture capitalists.

They relocated the company to San Francisco to expand and recruit engineering talent. Plaid now employs around 200 individuals, many of whom come together on Thursdays to go rock climbing. In case someone is stuck in the office, there’s also a climbing wall.

What is Plaid banking?

Plaid works as a bridge between your financial accounts and your eligible apps and services. Because of the complexities involved, Plaid believes it makes sense for these relationships to be managed by a third party. According to Plaid’s website,

“There are over 11,000 financial institutions in the United States, yet they organize and manage their data in a variety of ways. Building a digital connection to a single financial institution can take a lot of engineering effort and skill for an app that wishes to allow users to connect their bank accounts. Consider doing that a hundred times. It is not practical for many businesses.”

What customer data is shared by Plaid Banking with the linked companies?

When it comes to sharing data, plaid may provide the following data points to the company depending on the app or service you’re attempting to use, the kind of data shared, and the amount shared differs from company to company, so it does not apply to all.

- Account holder details: At a banking institution, they may request your name, address, phone number, and email address.

- Account transaction information: Balances, transaction dates, transaction kinds, and transaction descriptions are examples of data that may be exchanged.

- Account-specific information: Your account name or type, account number, routing number, and balance may all be shared data items.

If you use a single username and password to access numerous accounts, such as a checking account, savings account, and credit card, information from all accounts may be shared with the app or service you’ve chosen.

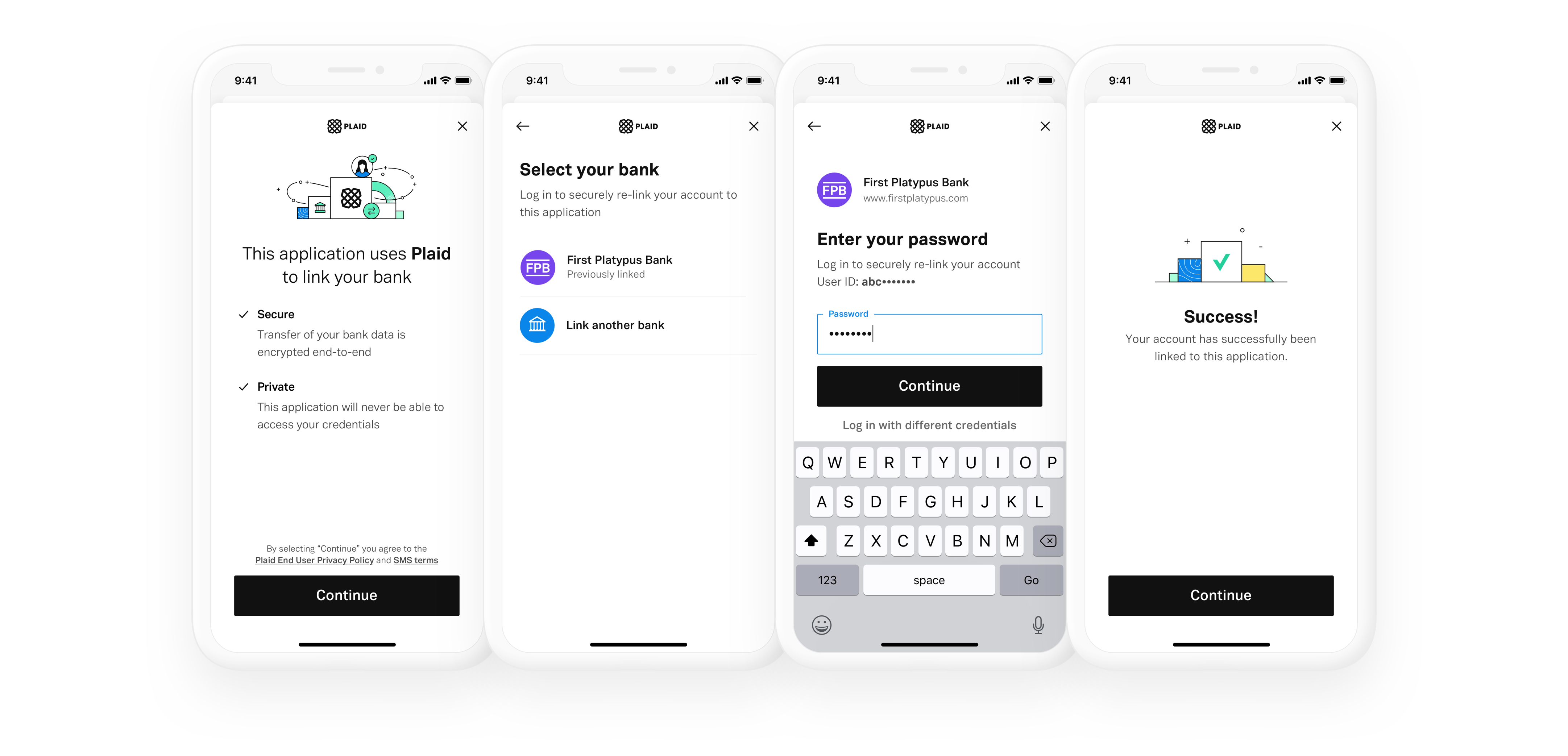

How does Plaid banking work?

Plaid banking operates without a standalone app or the need to create an account. Integrated within approved apps, Plaid enables you to add or link a bank account seamlessly. When prompted by an app, you’ll enter Plaid’s connection flow, which typically includes these steps:

- Choose or search for your financial institution.

- Enter your bank account login and password to authenticate.

- Verify data for security purposes.

- Select the financial accounts you wish to link.

- Complete the connection to the app or service.

For example, if you need to link your Chime bank or credit card account, Plaid facilitates this connection. A Plaid window will appear, prompting you to enter your Chime username and password. Plaid then uses this information to contact Chime and verify your login details.

If you have two-factor authentication (2FA) enabled, you’ll also need to input that information. Plaid offers its own 2FA option if your bank lacks this feature. Certified in internationally renowned security standards such as ISO 27001 and ISO 27701, Plaid is also SSAE18 SOC2 compliant.

Once you authenticate your bank information through Plaid, the established link allows for the transfer of permitted financial data, such as transaction history or balance. Recently, Sezzle, an installment payment platform, announced it would use Plaid for financial authorization. This partnership enables Sezzle customers to connect their financial accounts via Plaid, allowing them to pay more efficiently through the Automated Clearing House (ACH) instead of using a credit or debit card.

As a customer, you won’t be charged for using Plaid. The app needing the financial data exchange pays Plaid. However, not all accounts are eligible for connection. While Plaid’s network includes over 10,000 financial institutions, some accounts may not support or permit the third-party link.

How does Plaid make money?

Plaid primarily generates revenue through partnerships with financial institutions and service providers. Here are a few ways Plaid makes money:

- Transactions-based fees: Plaid charges a fee for each successful transaction made through its platform. This can include fees for account verification, balance checks, transaction data retrieval, and payment initiation.

- API access fees: Plaid offers developer tools and APIs that allow businesses to integrate Plaid’s functionality into their applications. Plaid charges fees based on its APIs’ level of access and usage.

- Enterprise solutions: Plaid offers customized solutions and support for larger enterprises and financial institutions. These solutions may include additional features, data analytics, and dedicated support, often provided under a subscription or licensing model.

- Premium services: Plaid may offer enhanced features, such as advanced data analytics, insights, or personalized financial management tools. These premium offerings typically come with a subscription fee.

- Partnerships and integrations: Plaid collaborates with various financial service providers, including banks, fintech companies, and payment processors. Through these partnerships, Plaid may receive referral fees, revenue-sharing agreements, or other forms of compensation.

These revenue streams allow Plaid to generate income and sustain its smooth operations.

Applications of Plaid

Plaid has a wide range of applications. These applications use plaid in various ways; it might be used to analyze your credit, validate your income, or certify sufficient funds for peer-to-peer payments. Some of the applications that use plaid are the following.

Venmo

You must input a username and password for an online bank account in order to authenticate a bank account on the Venmo mobile app for peer-to-peer payments and bank transfers through Plaid. To determine whether there is sufficient money to fund a transaction, Venmo uses that to check the account details and balance.

Chime

Another online-only financial application that Plaid facilitates is Chime. You can fund your Chime bank account using Plaid if you give it the login information for an acceptable external bank account.

Petal and TomoCredit

You might be requested to link a bank account through Plaid throughout the application process for the Petal credit card or the Tomo Card to provide a complete picture of your finances.

What benefits are there of using Plaid banking?

Plaid banking offers several benefits that significantly enhance the financial landscape for both consumers and financial institutions. Plaid’s advantages include decreasing fraud, expediting bank account identification, offering a detailed transaction history, displaying account balances in real-time, verifying borrower assets, and certifying user income. Plaid is a programming platform that aims to improve financial services. The following are some of its primary advantages.

Streamlined account connections

Plaid simplifies connecting bank accounts to various financial apps and services. It eliminates the need for manual entry of account details, reducing errors and saving time for users. This seamless integration allows individuals to access and leverage their financial data across multiple platforms effortlessly.

Enhanced financial overview

Plaid’s secure infrastructure facilitates the integration of innovative financial services. It enables the development of budgeting apps, investment platforms, lending services, and more. Through Plaid, users can access various financial tools and services that cater to their specific needs, expanding their financial capabilities and choices.

Improved ACH authentication

Authenticating accounts for bank-to-bank payments has been simplified, accelerated, and made more user-friendly. You’ll be able to rapidly authenticate transfers without having to wait for micro-deposits, and you’ll be able to eliminate unsuccessful transactions by authenticating and directing users to ACH.

Because you can set up users based on information they already know, this results in a seamless user experience, effectively reducing checkbook hunting. It also increases conversions by allowing you to use a mobile-optimized flow that converts considerably better.

Real-time balance checks

Plaid makes working with financial data easier. You may access historical data and real-time balances, current and available balance information, account status, and type details in just a few steps. You can instantly check your users’ balances whenever you need to make a transfer.

It aids in preventing overdrafts and allows for the pre-funding of transactions with balance visibility. Furthermore, visibility into available funds before transferring prevents non-sufficient fund (NSF) fines, decreasing, if not eliminating, fraud costs.

Reduce bank fraud

Plaid banking allows using bank data to verify identities and reduce bank fraud. You can verify user IDs such as name, phone number, address, and email and compare the information to what the bank has on file. You will be able to identify your users through a basic identity check, which will be aided further by auto-fill forms based on account holder information on file with the bank.

Transactions that are clean and well-organized

Money management becomes much easier when you have clean, categorized transaction data that goes back as far as 24 months. When combined with geolocation, merchant, and category information, you’ll have more detailed transaction information.

With reliable, real-time data that goes back as far as possible, you obtain vital insights to serve your customers better and save money with low-latency connections that don’t require additional technical resources.

Check borrower assets directly from the source

Borrowers can quickly link their bank accounts to optimize conversions. You receive rapid processing times with integrated technology that easily integrates Plaid into your own experience to eliminate borrower friction. The commitment to security, such as using enterprise-grade 256-bit AES encryption, which comes with regular network penetration tests and security reviews, also speeds up connections.

Data Security and Privacy

Plaid takes data security seriously. It utilizes advanced encryption and authentication protocols to protect sensitive financial information during data transfers. Plaid acts as a trusted intermediary, ensuring user data is securely transmitted between financial institutions and applications, mitigating the risk of data breaches.

Fostering Innovation and Competition

Plaid’s standardized APIs create a level playing field for fintech companies, encouraging innovation and competition in the financial industry. It enables startups and developers to build new applications and services, fostering a more vibrant and diverse ecosystem of financial tools for consumers.

Improved User Experience

Plaid simplifies the user experience by eliminating the need for multiple login credentials and manual data entry. It offers a seamless and user-friendly interface, enabling individuals to manage their finances across different platforms effortlessly. This convenience and ease of use enhance overall user satisfaction.

Plaid banking provides benefits such as streamlined account connections, a comprehensive financial overview, access to enhanced financial services, robust data security, fostering innovation, and an improved user experience. These advantages contribute to a more connected, efficient, and consumer-centric financial ecosystem.

Which banks are available on Plaid currently?

Numerous banks and online platforms use Plaid. To find out if your bank is protected, you can get the complete and updated information from the Plaid website. Here is a list of some of the options that are used by Plaid, which include well-known US banks and international financial services companies:

- Ally Bank

- Discover

- Capital One

- Santander

- US Bank

- Wells Fargo

- Bank of America

- TD Bank

- Vanguard

- American Express

- Barclaycard

Is Plaid banking safe?

Using Plaid banking is a secure way to utilize financial apps without giving the app access to your personal data. It extensively uses cutting-edge techniques to ensure the security and safety of its customers.

Plaid claims it takes the security of its customers’ data very seriously, as do most organizations that send financial information. Plaid employs encryption techniques such as the Advanced Encryption Standard (AES 256) and Transport Layer Security (TLS) when transmitting financial data. Knowing that your data is being transmitted utilizing these security settings may provide you with further assurance.

Plaid complies with a variety of other security best practices in addition to best-in-class security processes while managing data to keep your information secure. According to Plaid’s page on trust and safety

- If your banking institution does not provide enough security, it uses multi-factor authentication (MFA) to secure your account further.

- Plaid runs a bug bounty program to get extra eyes on security.

- Plaid promises not to share your data without your permission and not to sell or rent your information to other companies.

- It allows you to decide which businesses have access to your data and what information is shared with each of them.

How does Plaid protect your information?

Plaid puts you in charge of your personal data, ensuring you have full control. You have the authority to determine which details Plaid shares with applications, including,

- Balances

- Account and Routing Numbers

- Transactions

- Student loans

- Accounts profile information

- Investment holdings

- Credit card balance and interest rates

Rest assured, Plaid’s privacy policy explicitly states that your personal information will not be sold or shared. They solely utilize it to deliver the requested service, prioritizing your privacy and security.

Privacy concerns regarding Plaid banking

The total data users share with Plaid through many apps can be substantial. Therefore, users’ concerns about how the data is being utilized are undoubtedly legitimate.

Due to interface issues and excessive data collection, there were some concerns that Plaid decided to resolve by paying USD 58 million to Venmo, Robinhood, and other customers. Even though Plaid claims that the problem has already been fixed, they decided to settle.

Plaid’s website explains how it uses the data it collects and only does so with the user’s consent. You would, however, be aware from experience that consumers frequently need to remember to read the small print when joining up.

Therefore, it is in your best interest to read through Plaid’s Privacy Policy to understand how your data is saved and used by Plaid. Although it is challenging, you should read the section on how they use your information.

It is recommended to manage the connections by opening an account with Plaid and removing access as needed if you don’t want to give Plaid access to your data. Another option is connecting with apps that use Plaid using a different bank account.

How can you view apps linked to Plaid?

On my.plaid.com, you can register for a Plaid Portal account to manage some bank accounts connected to apps through Plaid. You may check the portal to see what kinds of data you’ve shared with other applications or services. According to the Plaid website, you can use the portal to disconnect applications or services from your financial accounts when you no longer want to share data and to remove any data that has been saved in its servers.

Why does Plaid request access to link my bank account?

Plaid connects to your bank account to establish a secure bridge between your financial institution and the applications that require financial information. This connection enables Plaid to retrieve specific data your financial apps need while safeguarding sensitive details. Plaid may retrieve information such as your account numbers for transactions, but it does so using encrypted tokens that protect your actual account information. Rest assured; Plaid prioritizes the security and privacy of your data.

What comes next for Plaid?

The acquisition of Cognito by Plaid contains a clue as to where it might go next.

Perret emphasized the importance of KYC (know your customer) protection as he described the agreement. Many financial organizations have stressed the importance of integrating robust and detailed fraud monitoring systems into their backend systems.

Perret said in an interview, “The truth is that our financial system was designed for a world without the Internet. And as a result, all of the technology has been retrofitted into a set of human-oriented procedures that are now mostly digital.”

It’s still quite gray whether Plaid would assist financial organizations with other stages of the onboarding process, particularly underwriting, because they “have such a plethora of data,” given the banking industry’s heightened focus on KYC. With Cognito’s help, Plaid can now identify a client’s customers and learn more about their specific demographics.

Controversies regarding Plaid

Plaid, a company known for its services related to user data, has been embroiled in controversy due to questionable practices. Some of these practices include.

- Gathering personal information without proper disclosure.

- Impersonating bank login screens.

- Scraping user data.

TD Bank even filed a lawsuit in 2020, accusing Plaid of attempting to deceive its users. In 2021, Plaid reached a settlement worth $58 million in a class action lawsuit. The lawsuit combined five separate cases into one, all alleging that Plaid collected and shared detailed financial information without obtaining consent from users.

The plaintiffs claimed that Plaid took advantage of its position as an intermediary. This settlement affects a significant number of people, approximately 98 million. Those who are eligible for the settlement can choose to receive the compensation automatically through popular payment platforms like PayPal and Venmo.

FAQs

Is Plaid banking secure?

Plaid takes security seriously and employs various measures to protect user data. It uses bank-grade encryption and follows the industry’s best practices to safeguard information. Plaid is also regulated and subject to data privacy laws and regulations.

Can Plaid banking be used with any bank?

Plaid supports connections with thousands of financial institutions, including major banks and credit unions. However, checking whether Plaid supports your specific bank before using its services is essential.

Are there any fees associated with Plaid banking?

Plaid provides its services to developers and financial institutions, who may choose to charge fees for their applications or services that utilize Plaid’s technology. As an end user, you may incur fees imposed by the specific application or service you use but not directly from Plaid.

Can Paid be used internationally?

Yes, Plaid supports connections with financial institutions outside of the United States. However, the availability of Plaid’s services may vary depending on the country and the specific financial institutions operating there.

Can Plaid banking be used for personal and business accounts?

Yes, Plaid supports both personal and business accounts. Users can link and manage multiple accounts across different banks and financial institutions through Plaid’s platform.

Can Plaid banking be integrated into my application?

Yes, Plaid offers developers tools and APIs (Application Programming Interfaces) that allow developers to integrate Plaid’s banking functionality into their applications, enabling them to access and utilize bank data securely.

Conclusion

Plaid, a fintech startup, connects over 4,500 businesses with consumers to third-party financial applications like Venmo, Acorns, Betterment, and many more.

When you use Plaid for banking with a third-party application, you authenticate with your bank’s official login details. The third-party app never sees your username or password. Instead, it only confirms that your login was successful and accesses the data you permit.

Even if you feel cautious about sharing your financial account details with a third party, Plaid emphasizes security as a top priority. Plaid never sells or rents your financial information. You have complete control over what data you share and with which companies.

You don’t need to create a new account or pay for the service if an app, service, or product requires linking an account through Plaid. By entering your approved bank account’s username and password, Plaid can connect and share your financial data according to the app’s guidelines.

Plaid remains a significant player in the financial apps ecosystem, utilized by numerous apps. As fintech applications evolve and integration expands, this list of connected services will only grow. Despite rising concerns over data security and privacy, Plaid’s simplicity and extensive use cases make it difficult to replace.

{kind=link}

{kind=link}